Current Issue

Without a history of credit, it is nearly impossible to receive a loan from traditional financial institutions. Banks typically heavily weigh someone’s credit score in assessing whether to issue a loan and in calculating the potential interest rate for said loan. If someone has no credit history then they have few alternatives for increasing their personal capital. Loans allow people to purchase homes, cars, start businesses, and many other features that increase a person’s standard of living.

This post explores how crypto companies are introducing a new way of providing loans and banking services; a method that is all-inclusive.

Traditional Method vs. Peer-to-Peer Lending

The traditional method of obtaining a loan can be intensive and lengthy; banks go through a number of steps to evaluate the likelihood that someone will pay back the loan. With a peer-to-peer network, an individual can receive a loan quicker, easier and with no intermediaries involved.

Peer-to-Peer lending is a method that allows everyone and anyone the ability to receive a loan. The typical crypto/peer-to-peer lending company accepts different types of cryptocurrency as collateral and loans the customer either cash or cryptocurrency in return.

While different companies such as BlockFi and ETHLend, all process and implement loans differently, the end product is relatively similar.

Structure of Crypto Lending Platforms

Not all lending platforms are structured the same way. An easy way to separate different types of lending platforms is to consider whether they hold the collateral with a third-party or on a smart contract. For example, BlockFi and Celsius Network both use third-party services to hold the collateral, while ETHLend uses smart contracts to hold the collateral for the duration of the loan Using a custodial services creates a more centralized loan platform since all collateral will be held by the company, while the use of a smart contract is similar to an individual agreement between a lender and a borrower.

Difference in How Interest is Calculated

One major difference between traditional bank loans and crypto lending platforms is how interest is calculated. Instead of using a FICO score, crypto lending companies calculate a loan-to-value ratio based on the amount of cryptocurrency the customer can use as collateral. The ratio is the principal amount divided by the value of the collateral. The biggest determining factor in obtaining a loan is how much crypto an applicant is able to put up as collateral. Different platforms calculate different interest rates based on the LTV of each loan. There is no credit score involved in the evaluation.

Legal Aspects of Lending Platforms

There are a few aspects that all lending platforms should follow in order to be compliant with current US laws. For instance, lending platforms should follow the Financial Crimes Enforcement Network (“FinCEN”) rules such as Know Your Customer and Anti-Money Laundering regulations. These requirements ensure that companies are doing their due diligence before engaging customers in a business transaction.

Essentially, blockchain companies that qualify as financial institutions must run a check on any customer before giving them a loan to ensure they are not a terrorist or engaged with certain countries. Most exchanges do not have clear policies about their adoption of FinCEN rules, but those that want to receive a BitLicense will need to adopt the policies.

Examples of Crypto Lending Platforms

BLOCKFI

BlockFi is an example of a central entity that works to issue loans to customers. In order to receive a loan, a prospective customer can use either Bitcoin, Gemini Dollar, or Ether as collateral. The paperwork is relatively quick and asks for some personal information, such as social security number, wallet public key, and bank information. Users are promised an answer to their loan within 24 hours. If the customer accepts the offer, they have to send their collateral to BlockFi, and BlockFi then transfers cash to the person’s bank account. At the end of the term, people can either refinance their loan or pay it off. The payments throughout the twelve-month period are interest-only, and a customer can pay back the interest in either Bitcoin, Ether, or USD.

In the event that the price of either Bitcoin or Ether decreases dramatically, and the LTV ratio increases to too risky of a percentage, BlockFi can take action and partially liquidate collateral in order to pay back part of the loan. At an LTV ratio of 70%, the customer is required to increase their collateral or payback enough of their loan to bring the loan to a 50% LTV. If the LTV ratio increases to 80% then BlockFi has the right to liquidate enough of the customer’s collateral to bring it down to a 70% LTV. BlockFi has a communication system in place to allow a customer up to 72 hours to either pay back part of the loan or to add more collateral to their loan.

The purpose of partially liquidating a loan is to prevent default. If a loan is automatically partially liquidated and those assets are used to immediately pay back part of the loan, then a customer can theoretically never default due to the fluctuating prices of cryptocurrency. This provides security to the company in the event that the price of any particular cryptocurrency drops dramatically.

BlockFi uses Gemini to hold its collateral and assets. BlockFi’s loan structure is fairly centralized but allows for rather seamless and secure lending from a nontraditional source.

CELSIUS NETWORK

Celsius Network is another centralized lending platform. Celsius uses BitGo as its qualified custodian. Celsius is attempting to act like a typical bank where customers can make deposits and withdrawals. It is important to note that Celsius does not put crypto funds in cold storage. The fund is able to earn interest and are used to pay loans to other customers and to invest (similar to an actual bank).

Celsius, in order to provide additional security to their customers and to protect their network, have a pool of assets from their fees to pay out any potential assets lost in a defaulted loan. This pool acts as an insurance in the event of a loss.

Additionally, Celsius has its own stable coin. Their stablecoin cannot be used as collateral but is accepted as a monthly interest payment. In the event of a fluctuation, Celsius will contact customers when the LTV is at 65% or higher. The customer then has twelve-hours to either add more collateral, pay back the loan, or be partially liquidated. In the event where the LTV increases to 80%, Celsius reserves the right to partially liquidate customers automatically until it returns to 70%.

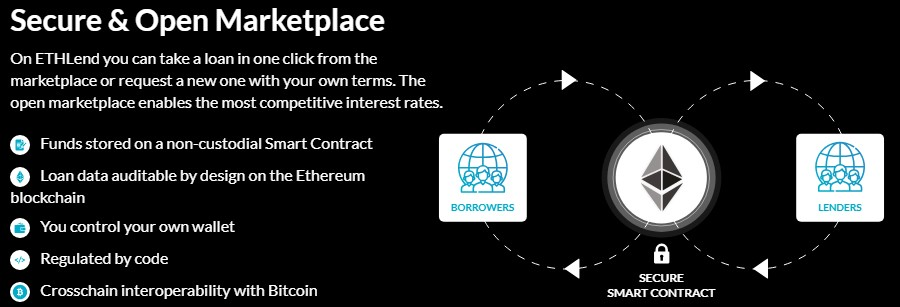

ETHLEND

Another way to structure a crypto lending platform is to act as an intermediary between borrowers and lenders and have no ownership for the loan. This more decentralized platform is employed by ETHLend. ETHLend is a platform that allows for both lenders and borrowers to find one another and execute loans through a smart contract. People who are looking for a loan can apply describing how much money they need, interest rate, number or installment payments, and the term of the loan. Once their desires are submitted, people who are willing to finance the loan are able to execute a smart contract. The main difference between the business structure of ETHLend and the other businesses discussed above is there no qualified custodian holding the assets for the duration of the loan. Here, these loans are extremely flexible but there is no guarantee that anyone will want to finance the proposed loan.

Recap

Blockchain-based lending platforms provide everyone and anyone an opportunity to obtain a loan. These platforms provide individuals multiple paths and multiple options in obtaining a loan. Further, these loans can be obtained in either fiat or cryptocurrency.

There is a large segment of people in the world without access to traditional financial services; these lending platforms are providing access to said services to those without.

HI dear

Wow, this is really interesting reading. I am glad I found this and got to read it. Great job on this content. I like it So we are provide Good Life Financial Hub’s vision is to provide.

Financial services in varanasi